I try to invest as much of my money as I can in the market because I’m a huge fan of compound interest and am focused on building my wealth. Personally, I keep my long-term investments at Wealthfront, where the 5-year return for a 9.0 risk score portfolio has been 11.94%1. However, the market can be volatile… that same portfolio would have been down by over 30% in just a few months in 2008 and 2020, but since those lows, it would have recovered and been up by ~400% and ~180% respectively. The key to benefiting from those recoveries was not having sold when you’re down and since I never know when the market might be down, I keep some money in cash for three reasons (I’ll talk about how much I keep in each later):

-

Regular expenses like mortgage, groceries and credit card bills

-

Emergency funds in case something large and unexpected comes up

-

Savings for big expenses in the next 3-5 years like a downpayment

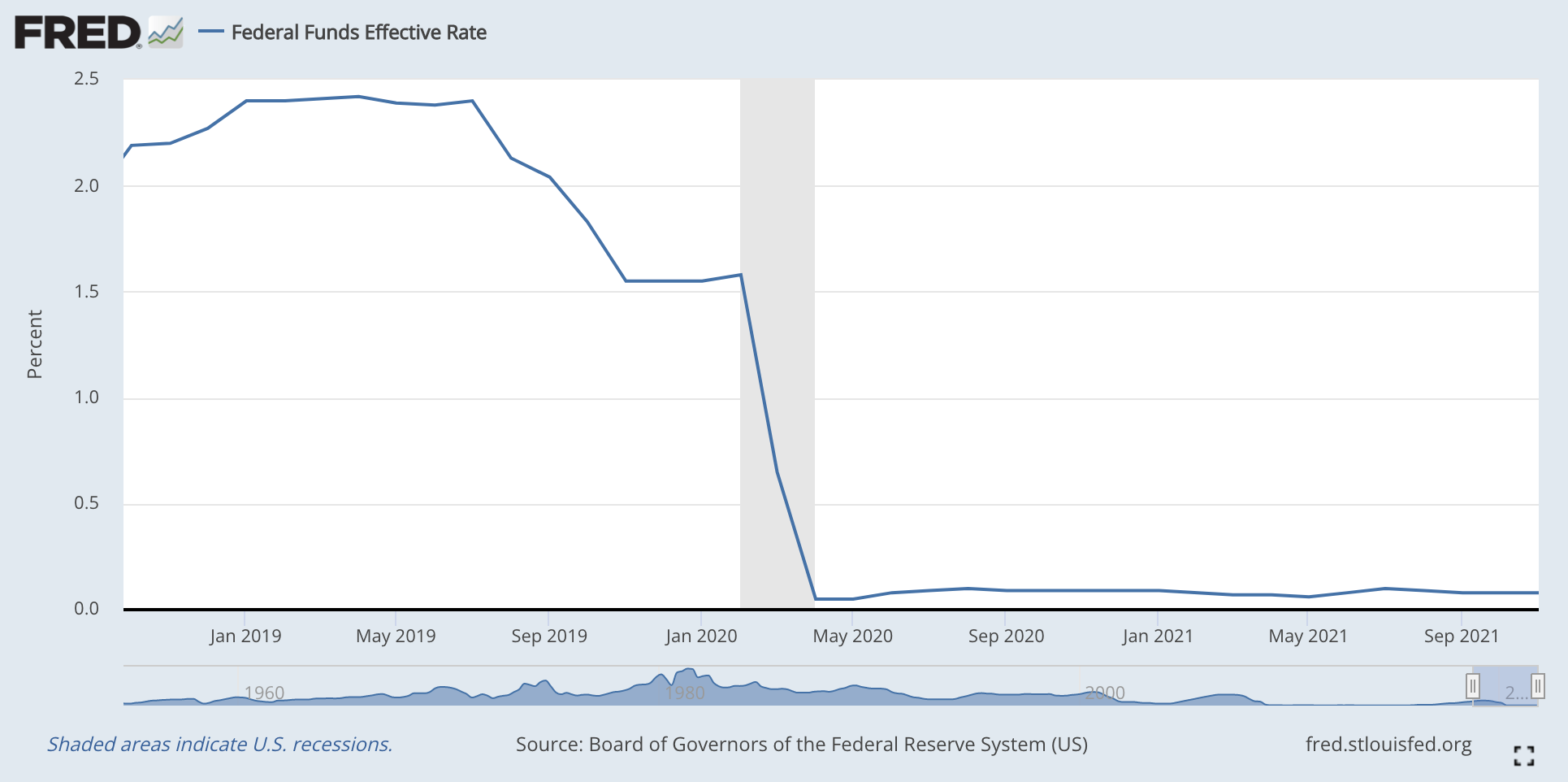

While I keep cash for regular expenses in my checking account where I don’t earn much interest, I want to keep #2 and #3 somewhere I can earn the most I can. Until the beginning of 2020 there were so many high yield savings accounts paying >2% interest. That was possible because the effective fed funds rate (EFFR), which is the average rate banks lend and borrow funds to each other, was above 2% for all of 2019.

That all changed in 2020 when the EFFR dropped to 0.05% (and hasn’t risen above 0.10% since), which meant that top online banks had to drop their rates and are now only paying 0.10-0.50% APY in their “high yield” savings accounts. That’s not just a problem because we all want to be earning more, it’s a problem because inflation (the increase in prices) is on the rise, hitting 6.2% in October (the highest level since 1990).

🏦 Where to Put Cash

So where do you put cash? I don’t want any restrictions on the account I use to pay bills each month, so I’m ok living with a low or no interest checking account. But where does the rest of the cash go? Here’s where I put my cash, along with one new option I’m considering:

-

Crypto Interest Accounts: Many crypto products have popped up here in the past few years, but the BlockFi Interest Account has now become the primary place I store cash. My deposits are automatically converted to USDC stablecoin and earn 9% APY accrued daily and compounded monthly. If you’re like me, you might wonder how this is possible. They generate interest by lending out your deposits to borrowers and because most large financial institutions aren’t tied into this ecosystem to lend money (similar to the cannabis industry) the rates are much higher. While most loans are overcollateralized, these accounts are not FDIC insured, so I would consider it higher risk than a traditional bank. However, despite multiple big crashes in the crypto markets, my account hasn’t been impacted once so it remains my primary place for cash. In fact, I’ve been such a fan of BlockFi for the last year that I reached out to them to see if they’d be interested in sponsoring the podcast. They said yes, so if you sign up with this link you can get up to $250 free. Also, I recorded an episode with the CEO of BlockFi to talk about how these accounts work, so if you want to learn more, you can listen here.

-

AA Miles Savings Account: Bask Bank offers an FDIC-insured savings account, but instead of paying $ interest, they pay American Airlines miles at a rate of 1 mile per dollar per year. With AA miles valued at 1.4¢ that’s an effective APY of 1.4%, but here’s the kicker: for tax purposes, Bask only values AA miles at 0.42¢, so if you assume a 35% marginal tax rate you could argue that the effective APY is 1.93% because you’re paying less taxes. I like having some miles with every airline and AA isn’t a transfer partner of any major credit card program, so I always keep some money at Bask to help boost my AA balance. However, keep in mind that if you don’t already have some AA miles you’ll probably need to keep at least $10,000 in this account to earn enough miles in one year for the cheapest award flights (e.g. one-way domestic).

-

Investing and not holding cash: This is a controversial one, so hear me out. Almost all of my long term investments are at Wealthfront, where I can take a PLOC loan against my portfolio for 2.4%. I also hold a few stocks at Interactive Brokers who offers the same option at 1.07%. Now, borrowing against your portfolio has a few major risks to call out: 1) your interest rate isn’t fixed and might go up at any time and 2) if the value of your investments falls significantly, you may receive a margin call and have to repay some of the loan to meet your equity requirements. However, if the amount you need to borrow is a small fraction of your portfolio, it’s much less likely that this will happen (example below). So, for short term needs during a low interest rate environment, where you have enough in your investment account that you’d need to borrow a small percentage of your portfolio, this might be a viable alternative to cash. For me, it’s replaced holding a large emergency fund in cash.

-

Example: If you had $100,000 in a Wealthfront portfolio and borrowed $25,000, you wouldn’t need to make a repayment unless your portfolio dropped ~60% to $40,000, which I don’t think has ever happened in my lifetime for a globally diverse passive index fund portfolio.

-

-

High Yield Savings: Yes, they might not pay enough interest to beat inflation this year, but they’re FDIC insured and the safest place to put cash. I only keep a small amount in a few of these accounts to ensure the account isn’t closed, in hopes that interest rates rise again soon. The bank with the best rate changes almost daily and most comparison sites prioritize whoever pays them the most. I think the best place to find the banks with the highest rates is Doctor of Credit. Two important things to keep in mind: 1) an extra 0.1% on $10,000 is only $10/year, so depending on your balance it might be better to focus on whatever bank is most convenient or offers the features you need (e.g. Wealthfront makes it fast to transfer to my investment account and Ally makes wire transfers easy) and 2) you don’t earn interest while your money is in transit, so chasing the best rate might actually hurt you (explained in more detail here).

-

LifeGoal ETFs: I’ve always struggled with giving friends a recommendation for an easy place to save for goals like a downpayment that keeps up with inflation but isn’t as risky as putting it all in the stock market. I recently came across LifeGoal Investments and am intrigued by their model. They offer a handful of ETFs, each designed specifically for goals like a child, downpayment or vacation. But most interestingly, a big part of the stock allocation in each fund is invested in companies they found to be correlated with that specific goal. For example, the largest holdings in the home downpayment ETF are Lowe’s, Home Depot and Zillow, which they hope will all be correlated with home prices and thus help your portfolio grow more if housing prices rise. They’re not a sponsor and I haven’t done enough research to endorse them, but it’s something I was excited to check out.

📊 How Much Cash To Hold

Using the three reasons I mentioned at the beginning of this email, here’s how much cash I hold for each:

-

Regular expenses: I typically only keep ~2x my average monthly spending in cash, however, my spending has been fluctuating quite a bit recently with a big family holiday trip and furnishing our home, so I’m now keeping a larger buffer (~4-5x monthly spending) of cash in my checking account. In a few months I hope to get back to ~2x and invest the extra cash.

-

Emergency funds: I like to make sure I have easy access to 6x my average monthly spending without selling my investments. However, as I mentioned earlier, I’m comfortable relying on a portfolio loan for emergencies, so I’m not currently holding any cash for this purpose.

-

Short Term Goals: This amount is entirely dependent on the major expenses you have planned in the next 3-5 years. For me that includes a downpayment for a new car next year, the au pair agency fee we’ll owe in January and some planned expenses for the show. I keep ~90% of this money at BlockFi and 10% at Bask Bank.

I hope all this was helpful, but I’ll be doing a Q&A episode on money, savings and investing soon, so please send any follow-up questions (or really any questions) my way by just replying to this email.

1) https://www.wealthfront.com/historical-performance

The content on this page is accurate as of the posting date; however, some of our partner offers may have expired.

Editor’s Note: Opinions expressed here are the author's alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.